Social Security has several features that make it extremely valuable, such as cost of living adjustments, guaranteed lifetime income for you and your spouse, and finally favorable tax treatment. Retirees can increase their after-tax income in retirement by understanding how Social Security income is taxed.

In 1983, President Ronald Reagan signed into law a new tax that would apply to social security income. Before 1983, retirees were not taxed on their Social Security benefits received in retirement. But because the Social Security Trust Fund was running low on money, lawmakers proposed taxing part of the benefits and putting the tax money back into the Social Security Trust Fund to help keep the program financially stable. The new tax law aimed to protect lower-income retirees from the new tax by specifying income levels below which retirees would not pay the new tax. This tiering of taxation has been adjusted over the years, but the original intent of limiting taxes for lower-income retirees has remained in place. Under current law, retirees will receive at least 15% of their Social Security income tax-free. However, depending on your income, you can receive up to 100% of your Social Security tax-free. This is where the Social Security Provisional Income Tax Rule comes into play.

The Social Security Provisional Income Tax Rule is a calculation used to determine whether or not your Social Security benefits are subject to federal income taxes. The calculation takes into account three types of income: your modified adjusted gross income (AGI minus Social Security benefits), any tax-exempt interest, and half of your Social Security benefits.

The formula for calculating your provisional income is as follows:

Provisional Income = Adjusted Gross Income (not including Social Security) + Tax-Exempt Interest + 1/2 of Social Security Benefits

To understand how the provisional income tax rule works, let’s break down each of these types of income:

Modified Adjusted Gross Income (MAGI)

Your “modified adjusted gross income” for Social Security tax purposes is your total income minus certain deductions. To calculate this figure, first determine your adjusted gross income, or AGI, for short. Your AGI includes your wages, salaries, and tips, as well as any interest, dividends, and capital gains you may have earned throughout the year. More commonly for retirees, it also includes any retirement income you may receive, such as a pension or distributions from a 401(k) or IRA. If you included any Social Security benefits in your AGI calculation, you will need to subtract that amount.

Tax-Exempt Interest:

Tax-exempt interest is any interest you earn from investments that are exempt from federal income tax, such as municipal bonds. Tax-exempt interest is normally excluded from federal income tax but you will need to add it back in to calculate provisional income.

Social Security Benefits:

Half of your Social Security benefits are included in your provisional income calculation. To calculate this amount, you take your total Social Security benefit amount and divide it by two.

Once you have these three pieces of information, you can use the Provisional Income Tax Rule formula to determine if you owe taxes on your Social Security benefits.

Once you have calculated your provisional income, you can then determine if your Social Security benefits are subject to federal income taxes. The amount of Social Security income that is tax-free also depends on your filing status.

Single Filers:

If your provisional income is between $25,000 and $34,000, up to 50% of your Social Security benefits may be subject to income taxes. If your provisional income is above $34,000, up to 85% of your Social Security benefits may be subject to income taxes.

Married Filling Jointly:

If you and your spouse file a joint tax return, and your provisional income is between $32,000 and $44,000, up to 50% of your Social Security benefits may be subject to income taxes. If your provisional income is above $44,000, up to 85% of your Social Security benefits may be subject to income taxes.

Here is an example to illustrate:

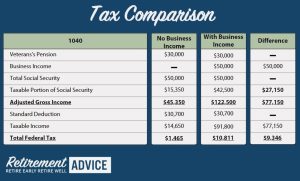

Say hello to Frank and Estelle Costanza. Frank Costanza and a family friend recently started a successful business selling specialty men’s garments, and Frank wants to know if the additional income will impact the taxes paid on his Social Security income. Frank and Estelle had the following income for the year:

Social Security: $50,000

Veteran’s Pension (Frank served in Korea): $30,000

Business Income: $50,000

Frank is surprised by the additional taxes he has to pay on his Social Security income as a result of his expanding business. Let’s look at a breakdown of the Costanza’s taxes with and without the extra business income:

The extra income made a significant impact on the Costanza’s taxes. Looking at the Difference column, their taxable Social Security increased by $27,150! Not only will the Costanzas have to pay taxes on this income, but they will do so at a rate of 22% compared to their previous marginal tax rate of 10%. This increase in taxes is referred to as the “Social Security tax torpedo.”

So what can retirees do to avoid the Social Security tax torpedo? Ultimately, anything a retiree can do to reduce their modified adjusted gross income can help. For example, a retiree who is over 70.5 and wants to help a charity could make the donation via a Qualified Charitable Distribution. Another idea is to proactively convert pre-tax retirement accounts to Roth accounts before required minimum distributions kick in at age 72. However, any Roth conversion plan or other tax strategy should only be implemented after a careful analysis to ensure the strategy actually makes sense for your situation.

Factoring in Social Security taxation to your retirement planning strategy can start well before you retire. You can benefit from evaluating how your Social Security could be impacted by taxes, whether you are already retired or working hard to retire in the next few years. For example, someone hoping to retire in their 50s or early 60s might map out their retirement income plan to determine how much they should be contributing to Roth vs. traditional retirement accounts.

Mark Whitaker, CFP® is a Certified Financial Planner™ professional, but he is not providing specific investment advice through this blog. This blog is for educational purposes only. Before making any financial decisions, you should consult with a qualified financial planner who can provide tailored advice based on your individual circumstances. Please visit https://earlyretirementadvice.com/online-booking/ to schedule a free one on one retirement consultation.